Understanding the Basics of Disability Insurance: What You Need to Know

Disability insurance is a crucial financial product designed to replace a portion of your income in the event that you become unable to work due to a disability. Understanding the basics of this insurance can help you make informed decisions about your financial future. There are two primary types of disability insurance: short-term and long-term. Short-term disability insurance typically provides benefits for several months, while long-term disability insurance can offer coverage that lasts for years or until retirement age. Knowing the differences between these two types is essential to selecting the right policy for your needs.

When considering disability insurance, it's important to evaluate several key factors:

- Coverage amount: How much of your income will be replaced?

- Waiting period: How long will you have to wait before benefits kick in?

- Policy duration: How long will you receive benefits if you become disabled?

Top 5 Myths About Disability Insurance Debunked

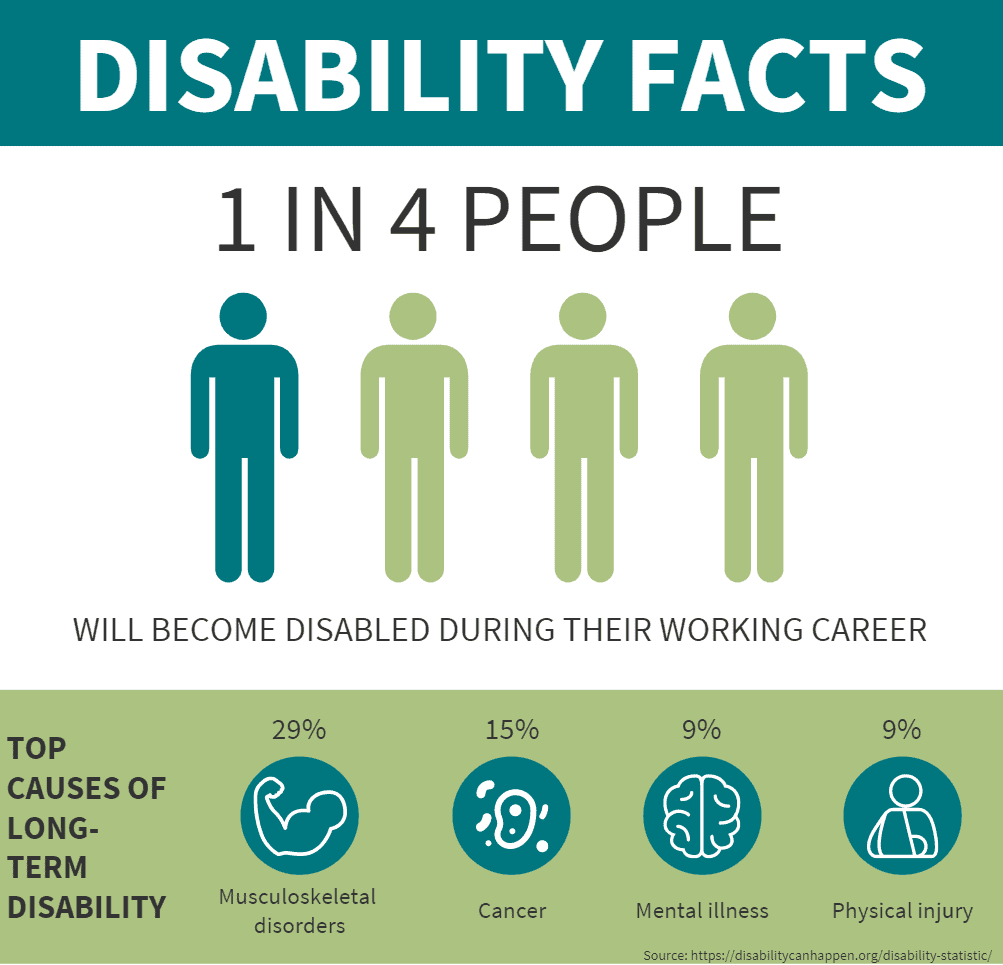

Disability insurance is often surrounded by misconceptions that can prevent individuals from making informed decisions about their financial security. One common myth is that disability insurance is exclusively for those in high-risk jobs. In reality, anyone can suffer from a disability due to accidents or illnesses, making it essential for all workers, regardless of their profession, to consider this form of protection. According to studies, a significant number of disabilities arise from non-work-related incidents, emphasizing the importance of having coverage in place.

Another prevalent myth is that disability insurance only pays out for workplace injuries. This isn't true; most policies cover disabilities caused by a range of factors, including chronic illnesses, mental health issues, and accidents, whether they occur at work or outside of it. Furthermore, many believe that disability insurance is too expensive and unnecessary. However, when considering the potential loss of income and the protection it provides, many find that the peace of mind is worth the investment. Understanding the facts can help dispel these myths and encourage individuals to secure their financial future.

Is Disability Insurance Worth It? Evaluating Your Options for Financial Security

When considering whether disability insurance is worth it, it's essential to evaluate your personal and financial circumstances. Disability insurance provides a financial safety net in the event that you become unable to work due to illness or injury. This protection can be invaluable, especially if you rely heavily on your income to support your lifestyle or family. Without this coverage, you may face significant challenges in maintaining your standard of living during times of unforeseen hardship.

To assess your options, consider the types of disability insurance available, such as short-term and long-term coverage. Short-term disability insurance typically provides benefits for a limited period, while long-term disability insurance can support you for years, or even until retirement age. Furthermore, analyze factors like coverage amounts, elimination periods, and premium costs. It’s crucial to understand what each policy entails so you can make an informed decision about how best to secure your financial future.